Table of Content

My prediction is that first home buyers the Reserve Bank will hold off on most bonuses for first home buyers.As discussed here, the low deposit borrowers are all but fully back in the market. If you search “nz interest rates forecast”, Google gives us 2.7 million results. Depending on what you paid for your home, you have a very good chance of making a profit in the 2019 housing market. No matter the market, the best time to buy a house is when you feel ready and have enough money saved for a down payment.

"They have historically trended to mirror the yields of U.S. Treasuries," explains Sharga. What actually happened is that mortgage rates began 2019 at approximately 4.75%. And some mortgage interest rates plunged below 3.5% in September.

NSB Mortgage Locations

Her writing has been produced internationally and she worked as an operations specialist in the Broadway touring industry. Keeping a close watch will make it easier to find and lock in a better rate. "If anyone could accurately predict them 51% of the time, they would be a billionaire. There are hedge funds with virtually unlimited resources trying to do this every day," adds McGrath. McGrath believes forecasting interest rates is virtually impossible. Rick Sharga, president/CEO of CJ Patrick Company, gave a "D+" grade to these 2019 predictions. James McGrath, co-founder of Yoreevo, gave a "C" grade to all the 2019 expert predictions above.

Mortgage rates have surged since the start of 2022, which reflects investors’ views that the economy is too hot and that the Federal Reserve will take any necessary steps to cool it down and rein in inflation. As far as which direction interest rates go in the years ahead, Fairweather expects declines. The average cost of a 15-year, fixed-rate mortgage has also surged to 5.78%, compared to 2.43% in early January. Before you start shopping around for a lender, you can find out how much you could save by using a mortgage refinancing calculator.

Home Loan Rates Are Forecasted to Remain Low: Plan Your Home Purchase or Refinance

I would like to see the government adjust the upper limits for the HomeStart Grant and the Welcome Home Loanhowever I don’t see this happening as Auckland property values are flat so there is no pressure to adjust. Even just making the criteria so it matched the KiwiBuild criteria would make the process of buying a first home a little less complicated. According to the same REINZ report, Wellington was up 9.8% (how is that for a prediction!). They predicted that the nation’s GDP growth will slow to a rate of 2.5% in 2019, followed by a rate of 1.8% in 2020.

While this inventory growth won’t push prices down in every market, there’s certainly a chance it could help in certain ones. In the majority of markets, the number of homes being put on the market or newly constructed has increased slightly, while the pace of sales has slowed slightly, which has helped stop the inventory decline. But the inventory increases or slowing price increases necessary for a more widespread sales gain are not forecasted to happen in 2019. While the situation is not getting worse for buyers, it’s also not improving notably in the majority of markets. It can be tricky to time any market, and mortgage rates are no exception. If conditions are choppy, and interest rates are likely to at least stay the same, if not rise, it may be smart to lock in a rate that works with your budget and seems fair to you.

Mortgage Rate Forecast for 2019 – 2020: A Modest Rise Ahead?

It isn’t just major metropolitan areas, either – one study found that home prices rose faster than wages in 80% of US markets. Despite these difficulties, millennials are purchasing the most homes, making up 45% of mortgages. As more millennials reach the peak home-buying age of 30, we’ll see that percentage increase in 2019 and 2020.

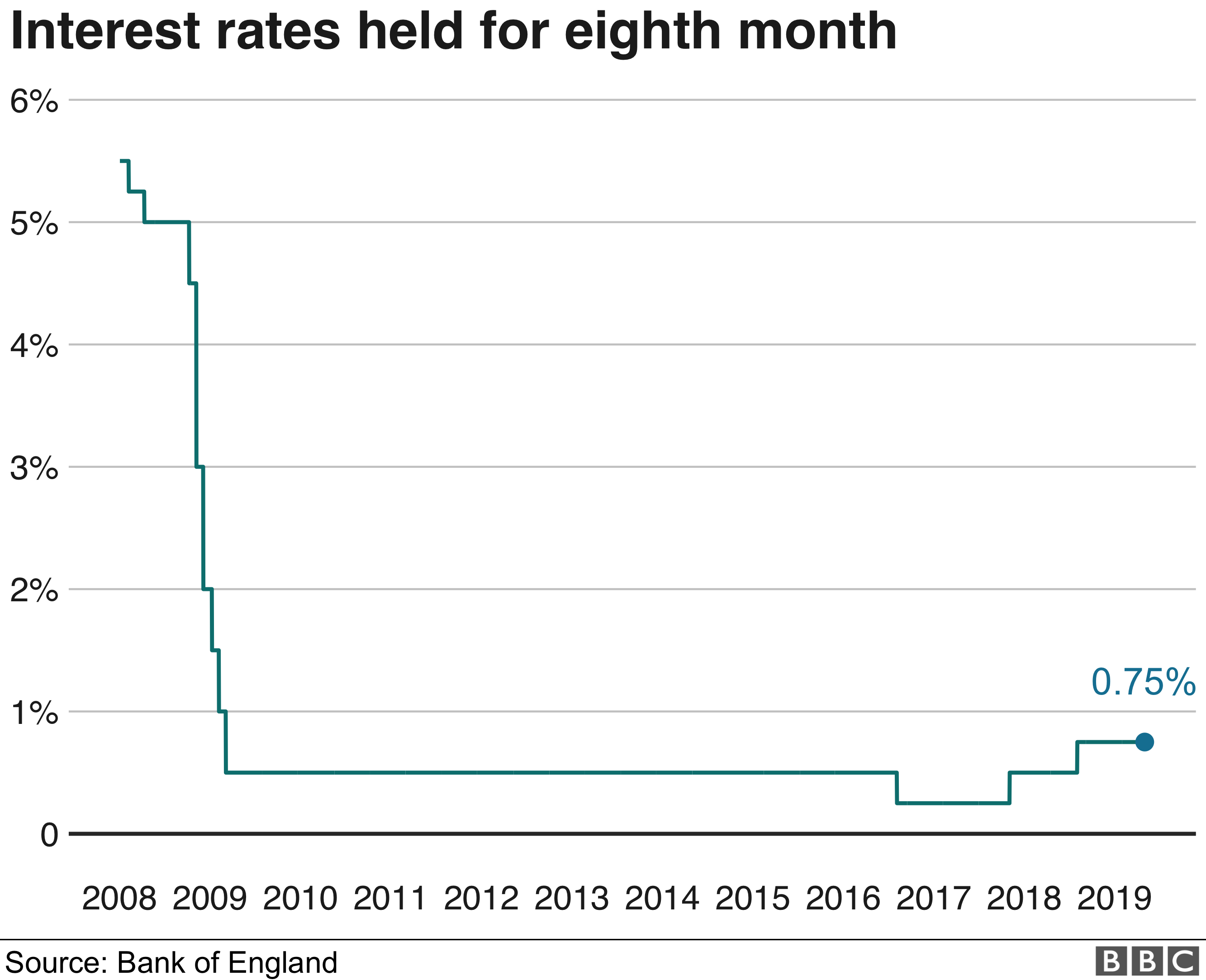

If money is a little too easy to get , the Reserve Bank may raise interest rates. If money isn’t flowing enough, then the Reserve Bank may lower interest rates. For some buyers, this reality means having to settle for a little less home. Keeping low balances on other credit lines and paying your bills on time will keep your score high and allow competitive rates to be part of your loan negotiation. This increase pushed average mortgage interest rates to nearly 5% in 2018.

These trends represent a great opportunity for borrowers who are planning to purchase or refinance a home in 2019. Home buyers, in particular, could capitalize on this by locking in a low rate for the long-term. This would essentially shield them from any mortgage rate increases that occur later in 2019, or beyond. Any student knows it can be constructive to look back and review your grades from the past year or semester. But the actual mortgage rates we got in 2019 were, in most cases, a lot lower than expected. The housing market forecast can play a big role in this decision – if housing prices are expected to rise, the dream home you’re barely able to afford now may become even more unaffordable down the road.

Unlike lead generation websites, we do not sell your information to multiple lenders or third-party companies. The latest Census Bureau data backs this up, showing single-family housing starts up 12.3% for the month and 6.6% over the year. I do expect rents to increase as the flow-through effects of ring-fenced losses, insulation requirements and even the recent Interest Only restrictions flow through to landlords. If you are in the market for a new home, learn more about your financing options today.

They don’t mention a specific rate in their 2019 Housing Market Outlook, just that rates on the 30-year fixed have been below 5% since the end of the Great Recession. That sounds pretty aggressive, especially in light of recent pullbacks in the stock market, but you never know. They’ve got a pretty boring 4.8% forecast for the 30-year fixed in all four quarters next years. Demographics still favorable – Even with a minor slow down, a strong job market and the pool of potential home buyers will keep the demand for homes higher than the supply can match. 30-year Fixed Mortgage Rates in the 4.0% to 4.5% range for most of the year. Also, worth mentioning that Fannie Mae is forecasting a year-end interest rate of 4.5% while the Mortgage Bankers Association is forecasting a 4.8% rate.

In general, the higher your credit score, the better your rate will be. To get an idea of where you stand, check your credit before you apply and dispute any errors with the appropriate credit bureau to potentially boost your score. You’ll also want to consider how long you plan on staying in your home as the closing costs can eat up your savings if you sell shortly after refinancing. The closing costs to refinance run between 2% to 5% of the loan amount, depending on the lender. So you should plan on keeping your home long enough to cover those costs and realize the savings from refinancing at a lower rate.

Rates did not drop below 5% until 2009 – and that was at the beginning of the financial meltdown. All three organizations expect home price growth to slow, reaching just a 2.2% appreciation rate by 2021, according to MBA. Last month’s House Price Index from the Federal Housing Finance Agency shows home prices were up 5% in July—down from the 6.7% uptick since just one year ago. Looking further ahead, the three organizations expect even more favorable conditions for 2020, predicting average rates as low as 3.4% . Now they’re calling for a total of $1.7 trillion loans to be made this year, and 72% of them being purchase loans.

Americans watch mortgage rates closely, and any time rates pull back even the slightest amount, more people apply for mortgages. With rates still substantially higher than a year ago, however, applications remain stuck near the lowest level in more than two decades, according to MBA data. "While long-term interest rate predictions might be far-fetched, it isn't impossible to see where mortgage rates are going in the short-term," says Gina Pogol, personal finance specialist with MoneyRates.com.

No comments:

Post a Comment